Learn why “Banking as a Marketplace” is the best route for product development.

Innovation in the financial services sector is not hard to find these days: predictive analytics for fraud, an AI-driven back-office, biometrics authentication. Now, a newer trend is coming to town. It does not have as much to do with the core banking technologies, but rather with how banks can change their business models through tech integrations.

So yes, rumor has it that the future of banking is a marketplace. Is it true? We very much believe so and have some data to back this up.

What is marketplace banking?

The marketplace banking model is an “ecosystem” of aggregated products and services sharing similar characteristics presented to the customer as a set of offers. It could be a set of various savings account options or custom insurance quotes.

Some banking marketplaces go one step further and fully integrate a host of services from another provider. For instance, a wealth management platform, an accounting app, or perhaps even a taxi-hailing functionality.

And this trend is growing stronger every day with banks like Monzo, Straling, Revolut, and others actively seeking partnership deals with other FinTechs and incumbent banks.

“We are building a banking experience fit for the 21st Century, where the best financial products are available securely in one place.” Megan Caywood, Chief Platform Officer at Starling Bank

But the idea of platform-based banking on a mobile device originally arrived from the East, where the “so-called” BAT (Baidu, Alibaba, and Tencent) triumvirate took over the retail banking sector in one quick swipe.

WeChat is the local “poster child” super app, showing how a tightly-knit ecosystem of financial, social, and lifestyle services can be neatly packed into one platform.

Using WeChat wallet, users can pay for a range of goods and services — both online and in real life. One quick QR code swipe and you are done with the checkout. Spending money online is even easier. WeChat payments are accepted by all major e-tailers. What’s even better, you often do not need to leave the app to get the thing you need.

In 2018, the mobile transaction volume in China reached $41.51 trillion. That is up by more than 28 times from 5 years ago. The People’s Bank of China (PBOC)

WeChat gives users access to over 1 million of carefully curated “mini-programs” – merchant accounts that you can transact with such as government services providers, celebrities, travel agencies, and more. While WeChat is not a traditional financial services provider per se, it does show how a “Bank as a Marketplace” model can thrive. So much so, that Facebook seems to be taking a very similar approach with their cryptocurrency-backed foray into the financial sector.

Product lessons FinTech banks should borrow from TechFins

After the initial phase of rapid customer growth, fostered by no-account fees, attractive mobile/online banking UX, and a seamless onboarding experience, challenger banks are now pressured to innovate to secure more users even further.

Their maturing customer segment is demanding additional services on-par with what traditional high street banks offer. Yet, packed into a better mobile “wrapper” and at a lower cost.

New product features and services can be “cooked” in-house. But should they when it’s becoming easier to integrate partners into your ecosystem instead of developing additional proprietary products?

Not really. Most customers will choose the “lowest-priced, most-trusted” option when it comes to commodity products such as credit cards, savings accounts, and general insurance. They do not care about the “brand” as much.

And that’s exactly the type of offers you can add to your digital banking ecosystem through partnership deals and third-party APIs. And with the arrival of Open Banking and PSD2, doing so would be even easier in terms of technology and compliance.

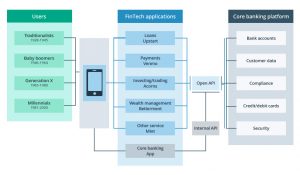

How to develop marketplace banking

Source: EY

The majority of FinTech startups already have a solid base – the core financial app – that is doing its job and fulfills all the basic financial customers’ needs.

The most progressive players are now shifting their attention towards delivering even more value to customers. And they are choosing to “outsource” more resource-heavy aspects of service delivery such as KYC, identity management, or regulatory compliance for new types of financial products to third parties.

Indeed, it makes perfect sense to build a marketplace bank if your goal is to deliver a more diverse product portfolio to customers for an affordable price and fast enough. By choosing the route of integrations, your team does not need to create a new infrastructure to support a certain offering. Instead, they can focus on devising additional value from the influx of customer data.

For customers, the appeal of platform banking is enormous too. Instead of being limited to a few selected products, they will be able to shop around in the digital banking “app store” and personalize their banking experience up to their needs — something the majority of consumers desperately lack.

85% of consumers name personalization as an important prerequisite for deepening their relationships with a bank. The Financial Brand

The best part? Your digital bank can expand beyond offering just financial services and become more of a one-stop-shop lifestyle product, covering all the users’ at the moment and long-term needs ranging from ordering a quick bite to saving up for a house and securing the best mortgage rate possible.

To get to this point, however, digital banks will need to do several things:

- Increase the level of process automation: Digitizing low-value manual operations and processes is the first condition for delivering bank capabilities through APIs.

- Switch to microservices architecture (unless already established) to enable seamless API communication between different application layers as well as with external vendors.

- Deploy Open APIs to enable integration with third parties.

- Build a continuous customer feedback loop with rapid prototyping and MVPs to rapidly test new ideas and understand which offers are working, which ones aren’t.

- Explore different integrations and partnership offers to keep in line with consumer demands and build up an ecosystem of value-added services.

The challenge for FinTech banks now is to decide which “goods” to curate at their marketplace.

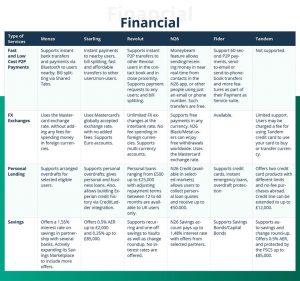

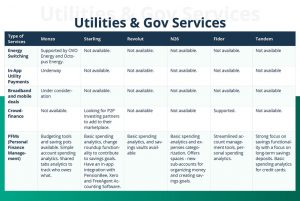

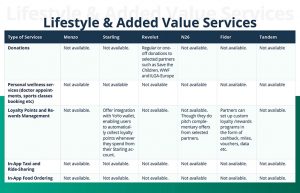

Below is a comparison chart showing which integrations the top banks are pursuing, along with some under-the-radar product development opportunities.

Banking marketplace comparison: what other digital banks are up to

The missing links in the digital banking marketplaces

As the chart indicates, most banks chose to concentrate their efforts on expanding their portfolio of financial services. Some are also venturing into the utility, insurance, and travel sectors. Yet, very few players are expanding beyond those areas – into the general lifestyle field.

And it’s a shame because this domain actually promises some massive rewards. Customers can definitely benefit from an added-value offered by their all-inclusive bank – grocery delivery organized regularly, travel insurance available, or a seamless in-app sign-in for a new gym.

Just consider the following data:

- Globally, the market for food delivery stands at €83 billion.

- The global travel booking market is expected to reach $1,955 billion by 2024.

- Wellness is now a $4.2 trillion global industry.

Your customers are already spending money on all those types of services. Enabling them to do so via your banking app means extra convenience for them, and an extra revenue stream for your business.

When you think of the current unicorn companies, you’ll find plenty of digital marketplaces on the list such as Airbnb, Uber, Coursera, and others. These companies did not revolutionize the industry with a brand new product per se. They capitalized on the “added value” obtained from offering a better way of connecting consumers with services providers.

As a digital bank, you can pursue a similar route — drive more value from offering your clients a better way to pick and choose the services they need.

Intellias has been a trusted software development partner for several FinTech players, pursuing the route of platformization. Contact us to learn more about how we can help you transform your digital bank into a marketplace.

Read the original article here