From Deloitte to HSBC, a host of players are once again drawing attention to personalization in banking. But how can you (and why should you) become a bank for one?

Delivering a personalized customer experience in retail banking is hard. Especially when you have many fires to put out amidst market uncertainty.

Crises come and go, channels change, and behaviors shift, but a retail bank remains profitable only if customer satisfaction and loyalty rates are high. These are metrics you can influence any day.

How? By providing an intelligent and tailored banking experience.

What is personalized banking?

Personalized banking services refer to the ability of a financial services provider to identify where customers are in their journey and present them with the most relevant financial products.

Or in the words of every other consumer: “It would be awesome if my bank could proactively help me manage my finances.”

To deliver a context-specific experience, banks can obtain an array of data points that indicate customers’ evident and underlying needs. Then they can link this data to big data analytics and machine learning models to churn out “next best action” predictions. The current state of technology allows that.

Machine learning, location-based services, and big data enable banks to anticipate customers’ needs and match them with major life events.

New Age in Banking Whitepaper by Intellias

Why personalized banking is the future of customer experience in finance

While banks possess a plethora of customer data, few use it to get personal. This is reflected in 2020 data from Accenture, which shows that only 29% of retail banking consumers trust their banks to look after their long-term financial wellbeing. Two years ago, the figure was 43%. Why such a tragic plunge?

The connected customer now expects more from their primary financial institution than knowing how to address them by name in a support chat or doling out an occasional personalized discount.

But bank customer satisfaction ratings among digital consumers remain low. In the US, the overall satisfaction score among digital-only retail banking consumers is 23 percentage points lower compared to branch-dependent customers.

This is a problem, as every forecast says that digital banking is here to stay. Up to 75% of bank customers plan to keep the digital banking habits they adopted during the pandemic.

Source: PYMNTS — Leveraging the digital banking shift

Source: PYMNTS — Leveraging the digital banking shift

Bank leaders acknowledge the need for action, with 84% naming “proactive engagement” and “personalized guidance” as key strategic goals for 2021.

Yet 25% of leaders in large banks and 50% in small organizations admit they have no tools to achieve these goals.

Here’s some reassurance for you: You’ve got what it takes to delight customers with a personalized banking experience.

All you need is:

- Customer data and a credit of trust to request more.86% of retail banking consumers say they are willing to share their data for a more personalized experience.

- Non-invasive analytics solutions that can co-exist with your legacy core.The ability to deliver personalization in banking doesn’t hinge on being a fully digital native company. While you will need to transform and upgrade certain systems, you are not required to lift and shift your entire core (at least for now).

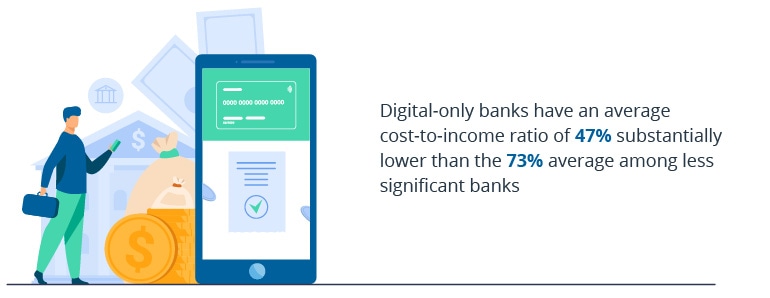

The best part? FinTechs and digital native banks have made significant advances in customer experience excellence and aggressive customer acquisition.

But they still trail banks in terms of the cost-to-income ratio due to more limited service portfolios.

Source: Deloitte — “Realizing the digital promise” report

A digital bank, on the other hand, has a wider portfolio of revenue-generating financial products. Reshuffle it based on customer needs to improve its performance.

How to get started with personalized banking

In a very basic sense, personalization means being present at the right time with the right offer.

A consumer in their late 50s may be more interested in building a cushion for retirement, while a 20-year-old wants to get out of debt faster while also building up funds for a rainy day.

Pitching 401K savings plans to both sounds fine on the surface. But far fewer 20-year-olds will take you up on this offer if they are underemployed or freelancers.

Personalization in banking empowers business leaders to distinguish primary target audiences from secondary audiences. Then companies can zoom in on each audience’s needs based on their financial status, lifestyle preferences, and life events. The above is a basic explanation of decision intelligence — wealth management banks are good at delivering for individual consumers and, sometimes, even en masse.

Retail bankers too can build digital indirect rapport with customers if they invest in the right technological frameworks. Here are the main steps to follow.

- Establish a data collection process

Banks already have plenty of data to use for personalization. The only constraint is enabling secure and compliant access to it.

That’s the challenge data governance addresses.

Data governance refers to a set of technical processes, practices, and policies that help financial institutions securely collect, manage, and use their data.

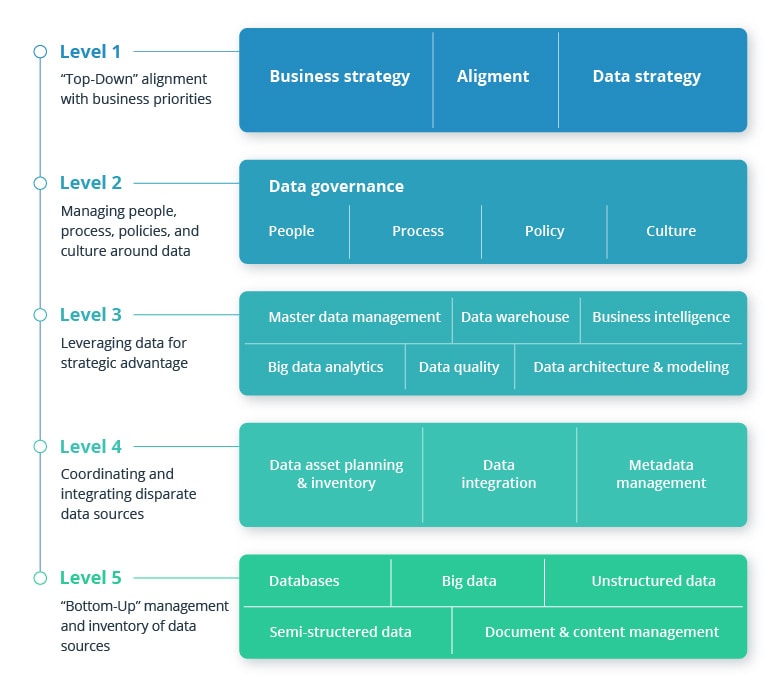

Aligning business and data strategy

Source: Dataversity — The Evolving Role of the Data Architect

Data governance helps to:

- Enable data collection from different sources

- Standardize data injection and storage formats

- Promote data quality and uniformity

- Establish unified data security and compliance standards

- Improve the state of data interoperability and integrations

- Unlock new data modeling techniques and approaches

As the chart above illustrates, you can use either a top-down or bottom-up approach to building a data collection process. In the case of personalization, you may want to start from the top down and inventory your data sources.

Data points to use for personalization in banking:

- Transactional information indicative of spending patterns

- Financial services and product usage data

- Demographics and CRM data as a proxy for customers’ lifestyle preferences

All of these insights are already stashed in your system. Your goal is to locate them and then create an integration for collecting, standardizing, cleansing, and storing insights in an analytics-friendly format.

Next, you’ll need a place to securely store those insights.

Most banking leaders go for a data lake or data warehouse. Both types of storage have technical merits for different types of analytics projects.

- Data warehousesare better suited for storing structured, transformed data you can plug into proprietary or custom analytics and business intelligence tools.

- Data lakescan house large chunks of big data in a raw state, meaning no extra manipulations are needed. They provide a range of intelligence that data scientists and machine learning experts can leverage for predictive models and AI algorithms.

- Connect extra data sources via APIs

You know your core banking systems. They may be past their prime, but they still serve a good purpose. Melding your core banking systems together sounds risky. Yet such systems often contain important data that can be used for personalization.

A viable solution is modernizing the necessary components only. Instead of breaking down the entire monolith, you can upgrade only several services to a microservice architecture. Then you can build a private API to connect them with your analytics system.

Apart from setting up internal APIs, you should also dip into the growing ecosystem of open APIs other industry players provide. By incorporating data from wealth management platforms, credit scoring apps, and other entities, you can learn about a wider range of your customers’ needs, preferences, and behavioral patterns (without sending yet another annoying survey).

- Mine customer intelligence

Customer intelligence refers to your ability to collect, analyze, and convert data into business knowledge.

From a technical standpoint, big data analytics and machine learning (going under the colloquial term “AI” these days) are the gateway for obtaining customer intelligence.

There are many predictive, prescriptive, and recommendation models you can use to transform the harnesses and organize data into customer intelligence for decision-making. The same models can be used to power the frontend banking experience for consumers.

When it comes to establishing a personalized banking experience, here are several options approved by consumers and industry leaders:

- Personalized digital account opening and customer onboarding

- Intelligent personal financial management apps

- Robo-investing and AI-driven wealth management products

- Behavior-based product recommendations, upsells, and cross-sells

- Accurate credit scoringand tailored lending product USPs

- Dynamic account pricing and service fees

- Micro-segmented marketing campaigns with better ROI

- Digital concierges and AI service advisors

No matter which personalization use case you decide to go for, one thing is certain: you will not only improve customer satisfaction and retention but also bump your revenues.

For every $100 billion in assets that a bank has, it can achieve as much as $300 million in revenue growth by personalizing its customer interactions.

BCG

Examples of personalized banking done right

It’s no secret that traditional retail banks lag in terms of customer experience and personalization, whereas digital players excel in this area.

According to McKinsey, among the 40% of consumers who use FinTech products every day, 90% are satisfied with their experience.

So what do digital native players do better than other retail banks?

Personalized customer onboarding

In terms of onboarding, the credit goes to Wealthfront. This wealth management platform balances UX best practices with data collection during the onboarding stage. Users are presented with an interactive questionnaire inquiring about their financial goals and lifestyle preferences.

Such a conversational experience helps the company collect all necessary information for KYC and connected personalization algorithms without turning the experience into a drag for prospective customers.

Personalized financial coaching

Credit Karma has taught a lot of users how to curb excessive spending and pay off debts. The company has developed a sophisticated predictive algorithm that captures over 2,600 data attributes per user. In a matter of seconds, it translates data into 8 billion predictions about what products or actions to recommend to the user.

Best personalized lending experience

Atom Bank is often praised for the interface customization it provides. From a recent design-your-logo campaign to card and account view customization, Atom does a lot to delight customers with design.

As landing as a service changing the financial services landscape, Atom Bank has made a progress in lending to stay competitive. The mobile bank has streamlined the mortgage application process. Now it takes 22 minutes to apply for a loan and the remortgage application takes just nine days.

To conclude

The above list just scratches the surface of personalization opportunities in banking, fueled by big data and machine learning algorithms. Consumers have cast their votes too — and they demand banking to be digital and personal.

Now it’s time to step up and deliver. Re-assess your product portfolio and make it serve your customers’ needs. There’s no need to go after multiple targets and magnify operational risks. Find an unmet consumer need. Analyze which financial products can best fulfill it. Then look for data sources and algorithms to personalize the experience.

___

Find out more about Intellias here.